Dry bulk capacity growth slows further, encouraging sign for later half of 2013

In a highly commoditized industry like the shipping industry, capacity is an important metric that directly impacts companies’ top line, or revenue performance.

When capacity grows faster than demand, competition will rise among individual shipping firms as they try to utilize idle ships and cover fixed costs.

This will lower day rates, which will negatively affect bottom line earnings, free cash flows and share prices for companies such as DryShips Inc. (DRYS), Diana Shipping Inc. (DSX), Navios Maritime Partners LP (NMM) and Safe Bulkers Inc. (SB).

Rise in capacity is the lowest figure, year-over-year, in week ending April 19th For the week ending April 27th, dry bulk ship capacity grew 6.95% year-over-year to 595.98 million dwt, lower than the 7.10% increase seen for the prior week.

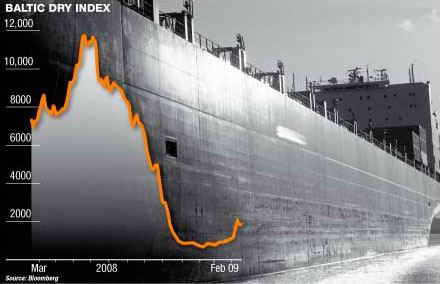

This is a large improvement since the beginning of 2011 when capacity growth was running above 16%, primarily driven by over purchases of new ship builds as managers became too optimistic with future trade growth before the financial crisis.

Unfortunately, trade growth fell after the financial crisis as the golden age of investment led economic development in China to come to an end. Growth in iron ore imports, which makes up more than ~20% of global dry bulk trade, fell from 17.8% to 5.7% per year. In 2013, Jefferies estimates signal expected dry bulk trade growth of at least 6%.

At the beginning of the year, dry bulk ship capacity grew at a rate of 9.46% year-over-year; last week, it was growing at 6.95%. The probability that demand growth will outpace supply growth later this year looks increasingly more promising.

Long-term outlook for dry bulk shipping looks positive While dry bulk firms, such as DRYS, DSX, NMM and SB, will continue to face headwinds in the short to medium-term, since China’s economic data appears to be less optimistic compared to the start of the year and capacity growth remains elevated, shipping companies should do well in the long-run as shipping rates are at a record low and should eventually recover.

For investors looking to diversify investments across several companies, they can look towards the Guggenheim Shipping ETF (SEA), which invests in the largest shipping companies world-wide. Source: Market Realist

In a highly commoditized industry like the shipping industry, capacity is an important metric that directly impacts companies’ top line, or revenue performance.

When capacity grows faster than demand, competition will rise among individual shipping firms as they try to utilize idle ships and cover fixed costs.

This will lower day rates, which will negatively affect bottom line earnings, free cash flows and share prices for companies such as DryShips Inc. (DRYS), Diana Shipping Inc. (DSX), Navios Maritime Partners LP (NMM) and Safe Bulkers Inc. (SB).

Rise in capacity is the lowest figure, year-over-year, in week ending April 19th For the week ending April 27th, dry bulk ship capacity grew 6.95% year-over-year to 595.98 million dwt, lower than the 7.10% increase seen for the prior week.

This is a large improvement since the beginning of 2011 when capacity growth was running above 16%, primarily driven by over purchases of new ship builds as managers became too optimistic with future trade growth before the financial crisis.

Unfortunately, trade growth fell after the financial crisis as the golden age of investment led economic development in China to come to an end. Growth in iron ore imports, which makes up more than ~20% of global dry bulk trade, fell from 17.8% to 5.7% per year. In 2013, Jefferies estimates signal expected dry bulk trade growth of at least 6%.

At the beginning of the year, dry bulk ship capacity grew at a rate of 9.46% year-over-year; last week, it was growing at 6.95%. The probability that demand growth will outpace supply growth later this year looks increasingly more promising.

Long-term outlook for dry bulk shipping looks positive While dry bulk firms, such as DRYS, DSX, NMM and SB, will continue to face headwinds in the short to medium-term, since China’s economic data appears to be less optimistic compared to the start of the year and capacity growth remains elevated, shipping companies should do well in the long-run as shipping rates are at a record low and should eventually recover.

For investors looking to diversify investments across several companies, they can look towards the Guggenheim Shipping ETF (SEA), which invests in the largest shipping companies world-wide. Source: Market Realist